YOUR ULTIMATE RESOURCE ON THE NEW

DIGITAL ECONOMY

Topics about Smart Cities, Fintech, Digital Marketing, Internet of Things, Social Media and Everything Else

by Yap Heng Kiong

|

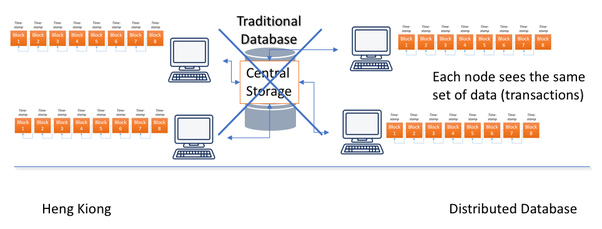

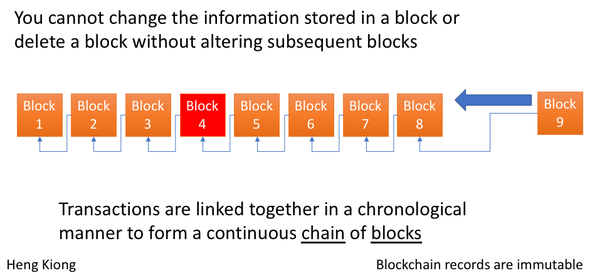

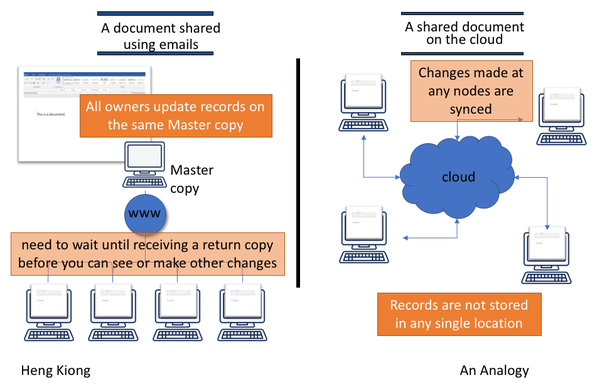

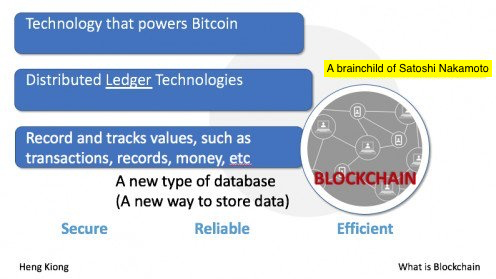

A blockchain is a cryptographically secure distributed ledger. Transactions (either money or records) are validated by complex computer algorithms. Verified transactions are “Chained” together in “Blocks” using cryptography. (that’s why the name Blockchain). In Blockchain, the ledger is not stored in any centralised server; but distributed via a network of computers. Each node sees the same set of data (transactions). Data is stored in ledgers across all nodes (hence distributed) in the Blockchain network. Ledgers are updated when there are new validated transactions. Additions to the Blockchain can only be made after validation using a Consensus Mechanism. The two most popular ones being Proof-Of-Work (PoW) and Proof-Of-State (PoS). This makes it extremely difficult for anyone to tamper with the data.  Can Data Stored on a Blockchain Be Erased? Each node on a Blockchain network has a verified, up-to-date and immutable history of all transactions. Once validated, transactions cannot be altered and cannot be tampered with. Data is reversible only by a subsequent transaction. What is the difference between a distributed database and a centralised database? A centralised database can be explained using the analogy of a document being shared among users via emails. All owners update records on the same Master copy. All parties involved would need to wait until receiving a return copy before one can see or make other changes. On the other hand, a decentralised database is like when multiple parties work on a shared document in the cloud, changes made at any nodes are synchronised. Blockchain uses decentralised database system (or distributed ledger), records are not stored in any single location. Once a record or transaction is stored on a Blockchain, it is extremely difficult to amend. I am creating a multi-part guide on the fundamentals of Blockchain. Part 1 and 2 have been released and can be found at below link.

Click here to access the guide Part 1 - What is Blockchain? Part 2 - Centralised vs Decentralised Database

3 Comments

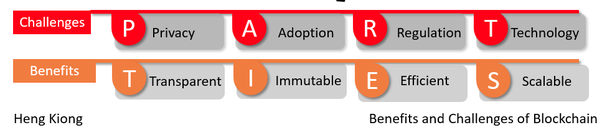

Blockchain is a network of computers (nodes) that can compute the authenticity of transactions in a decentralised manner. Due to its distributed database, Blockchain effectively cuts down on operational inefficiencies and ultimately saves money. Blockchains taps on existing proven technology concepts and mathematical functions to build a secure, immutable record of who owns what and when. This eliminates the need for third parties (intermediaries such as banks). Even though in the early stages of adoption, many believe that Blockchain can potentially reshape how businesses can be done around the globe. For example, in Logistics and Supply Chain, moving to Blockchain has potential to allow trades and transactions to become more efficient, especially across borders. In summary, Blockchain SIMPLIFIES workflow processes and REDUCES the cost of conducting business transactions. Benefits for businesses include:

Any industry striving to achieve better operational efficiencies and seeking to reduce cost of business are potential used cases for Blockchain. There is a nice picture I found online showing potential industry disruption: Newco Shift | Graphic: Blockchain for Every Industry Is It Difficult to Learn About Blockchain?Well it depends on to what level of competency you wish to master. Largely, I think we can divide into the following -

I am creating a multi-part guide on the fundamentals of Blockchain. Part 1 and 2 have been released and can be found at below link. Click here to access the guide Part 1 - What is Blockchain? Part 2 - Centralised vs Decentralised Database

Google Tag Managers are Tracking scripts you set up to place on your website to monitor web performance. Google Tag Manager saves time by letting you place tagging scripts on your own.

The following steps outline the process from setting up a Google Tag Manager (GTM) to installing and configuring to monitor your web performance. Using Google Chrome, goto https://www.google.com/analytics/tag-manager/ Setting Up A Google Tag Manager Account

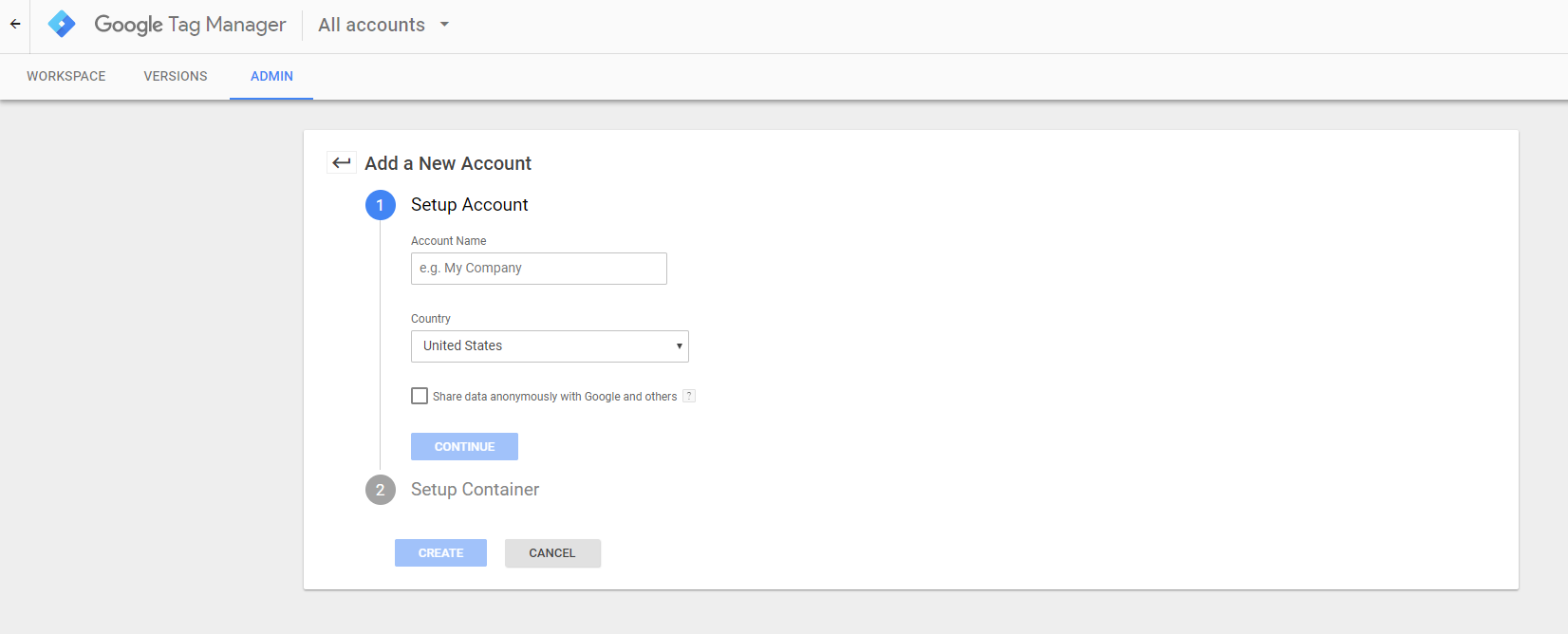

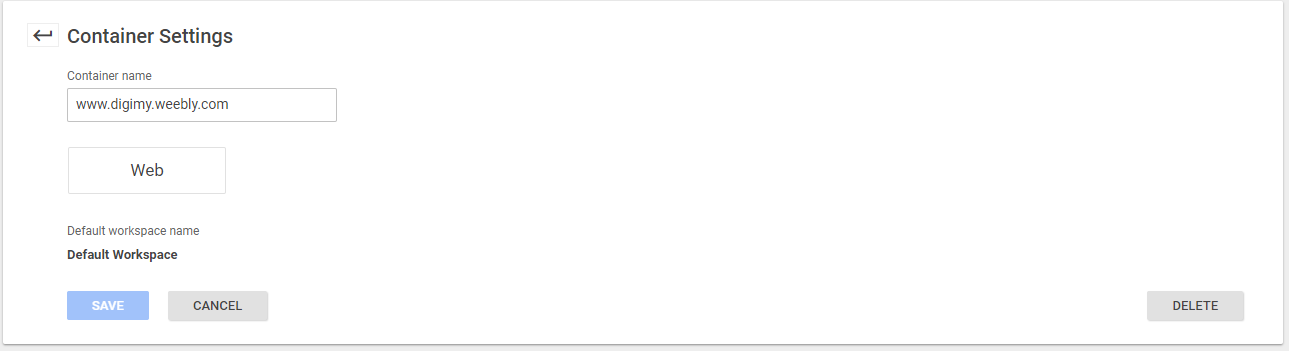

After logging in, add a New Account. This is where you set up your Account information and the types of Containers. Since I want to monitor the web performance for my own website, www.digimy.weebly.com, I set up the Container Settings as shown below.

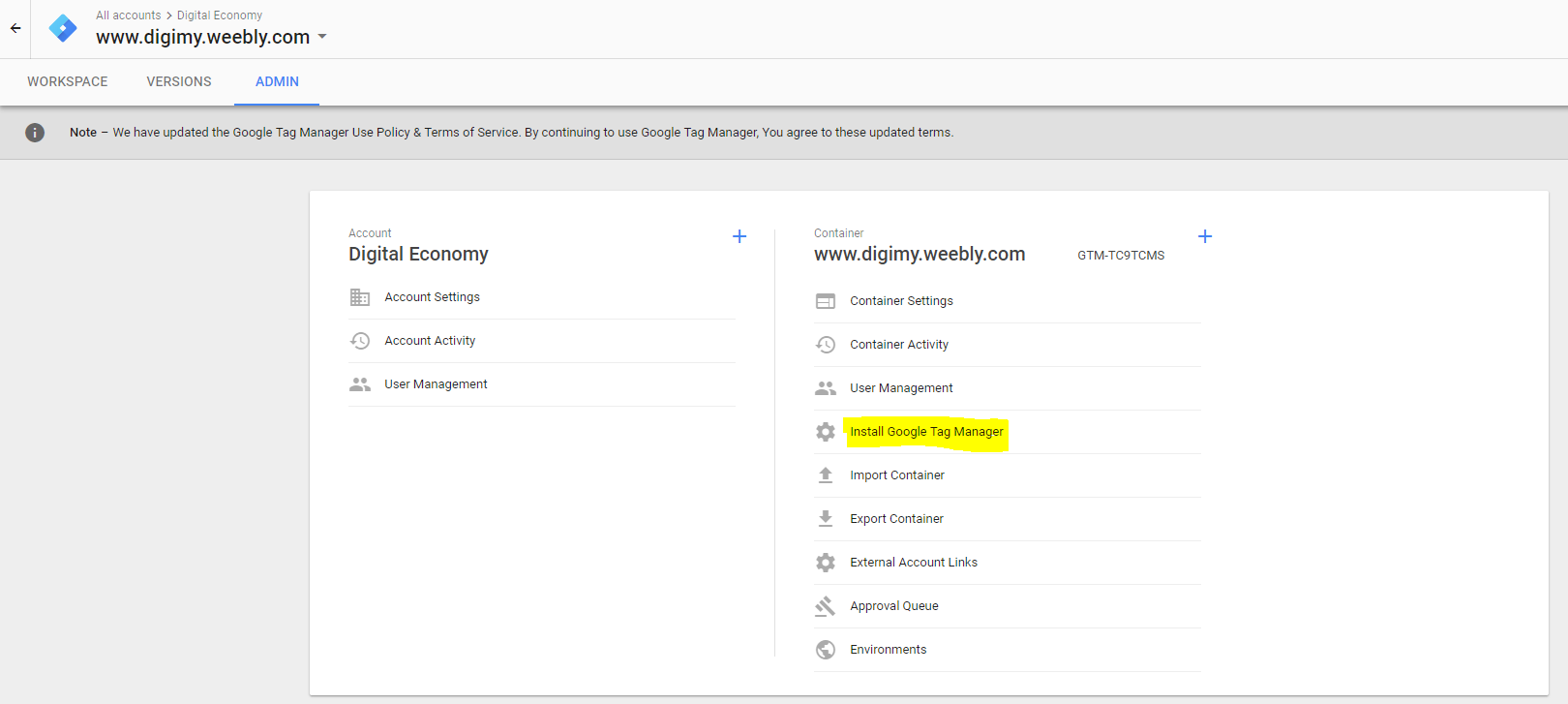

Next, still at Admin, choose Install Google Tag Manager.

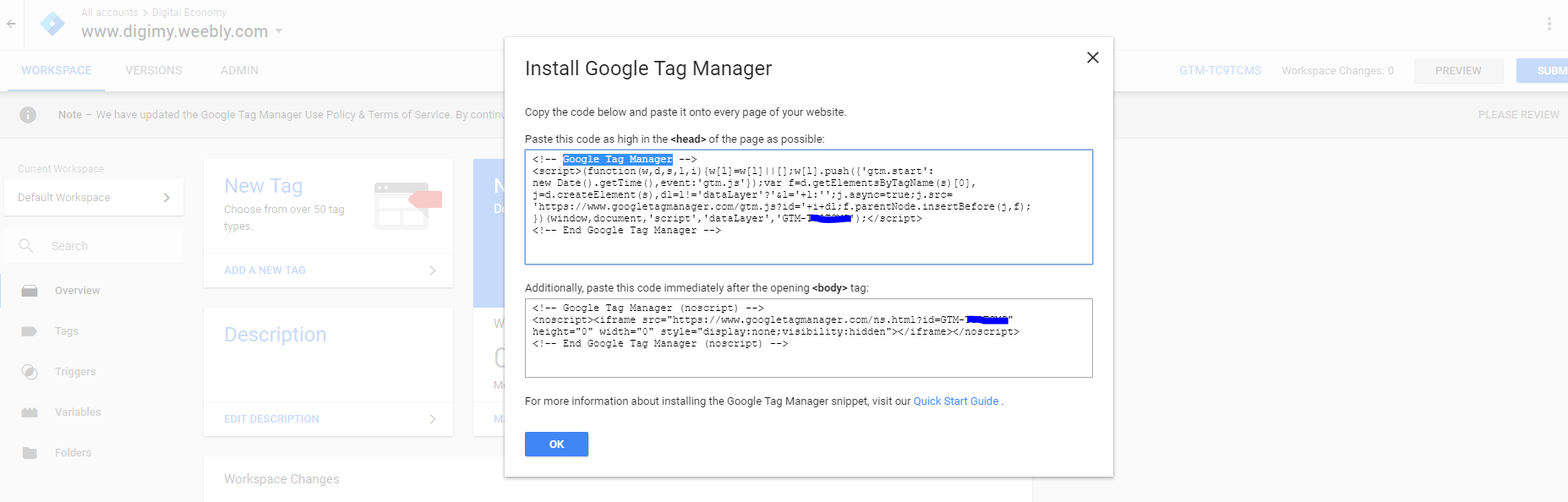

Copy the Tag Manager Codes onto your Website

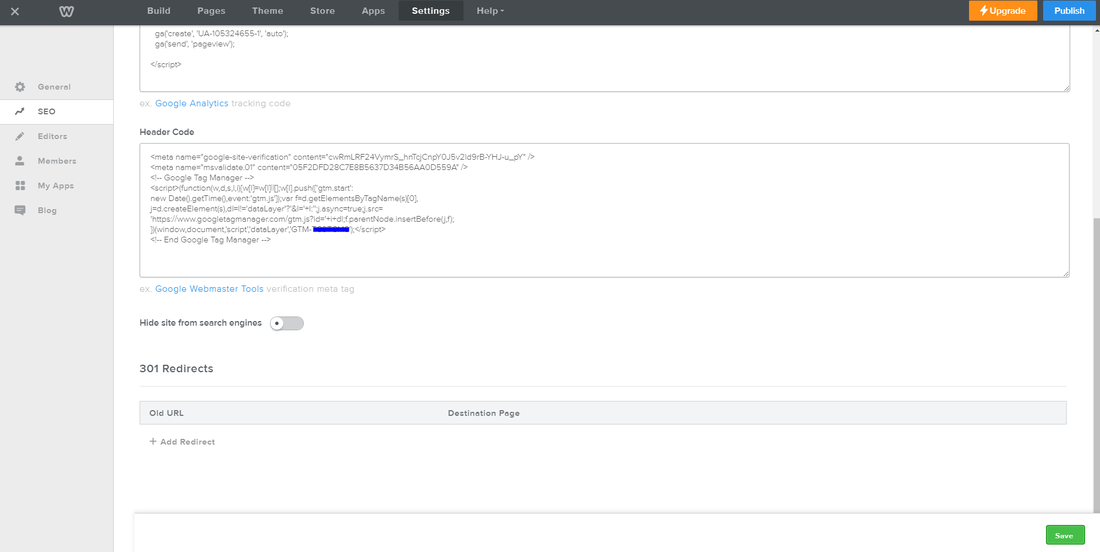

The first block of codes to be pasted as high in the <head> of the page as possible. As I am using Weebly for my blog, these codes will go to Settings > SEO > Header Code

Additionally, the second block of codes should be pasted immediately after the opening <body> tag of each page to be tracked. Hence, using the Embed Code element above all my other content of that page.

Creating an Universal Analytics Tag with GTM

First and foremost, obtain the Google Tracking ID by signing on to Google Analytics. Goto Admin setting, select the website you wish to track and click on Tracking Code under Property.

Copy down the Tracking ID starting with UA. You will need this later. Storing your Google Analytics Tracking ID with Variables

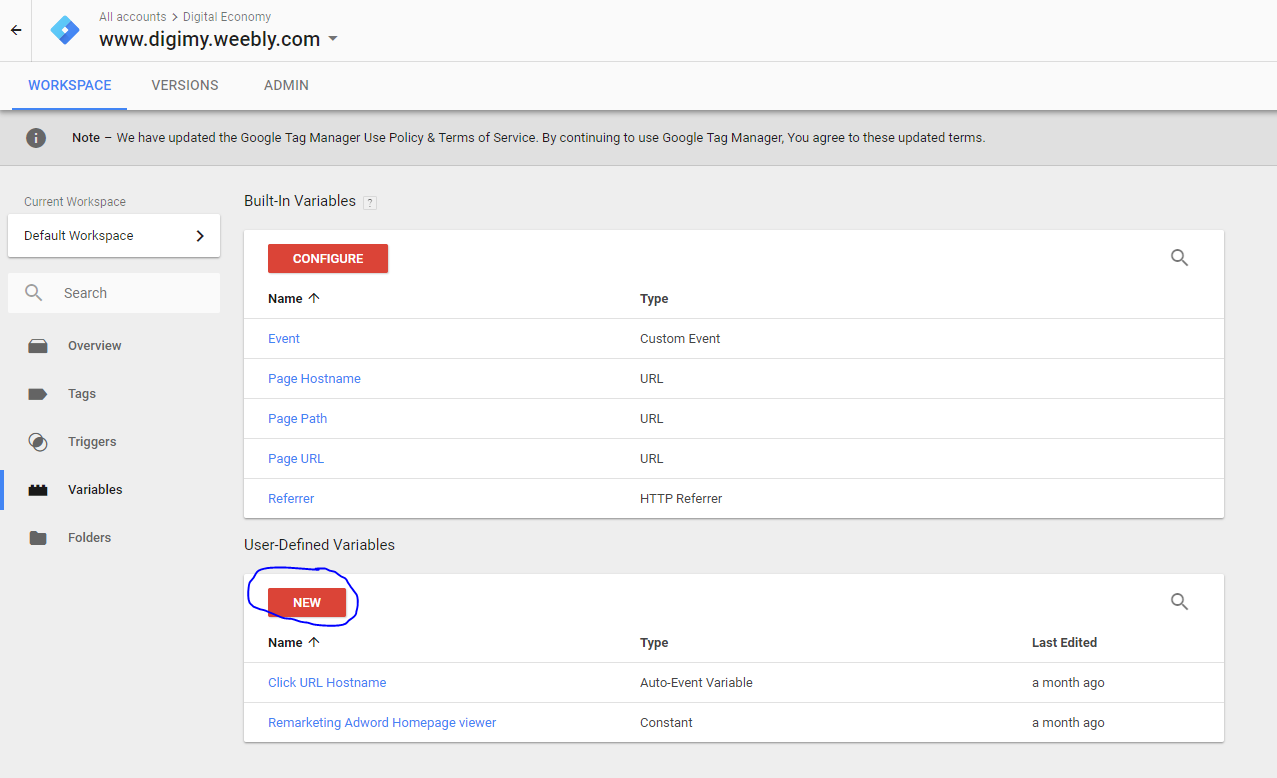

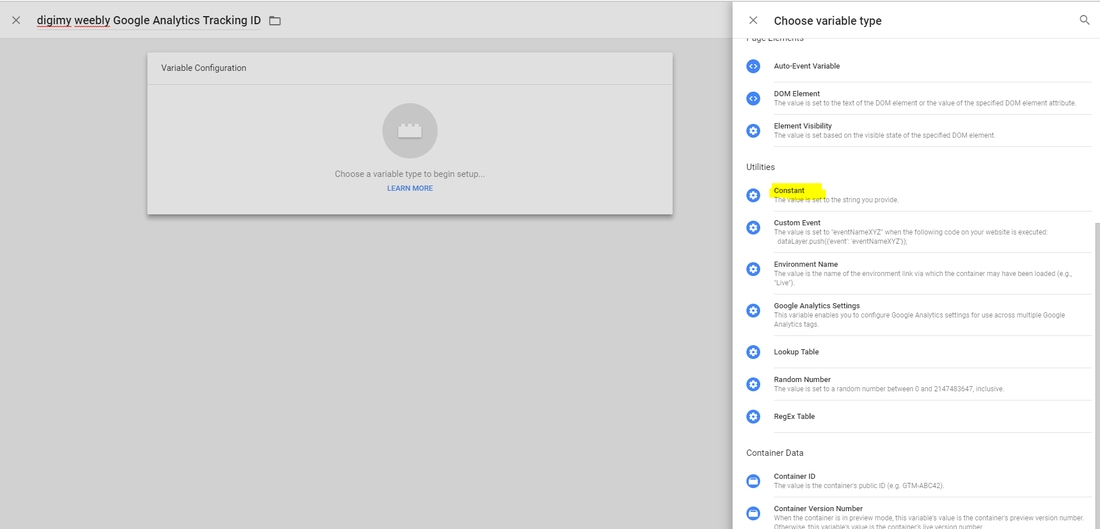

Instead of pasting the Tracking ID over and over again at Google Tag Manager whenever we set up a tag, I want to use the Variables option to store the Tracking ID. Click on Variables at GTM, and choose NEW Use-Defined Variables.

I want to name the new Variable as digimy weebly Google Analytics Tracking ID.

On the right panel, scroll down until you find Constant.

Paste the Google Analytics Tracking ID under the Value box and click on SAVE.

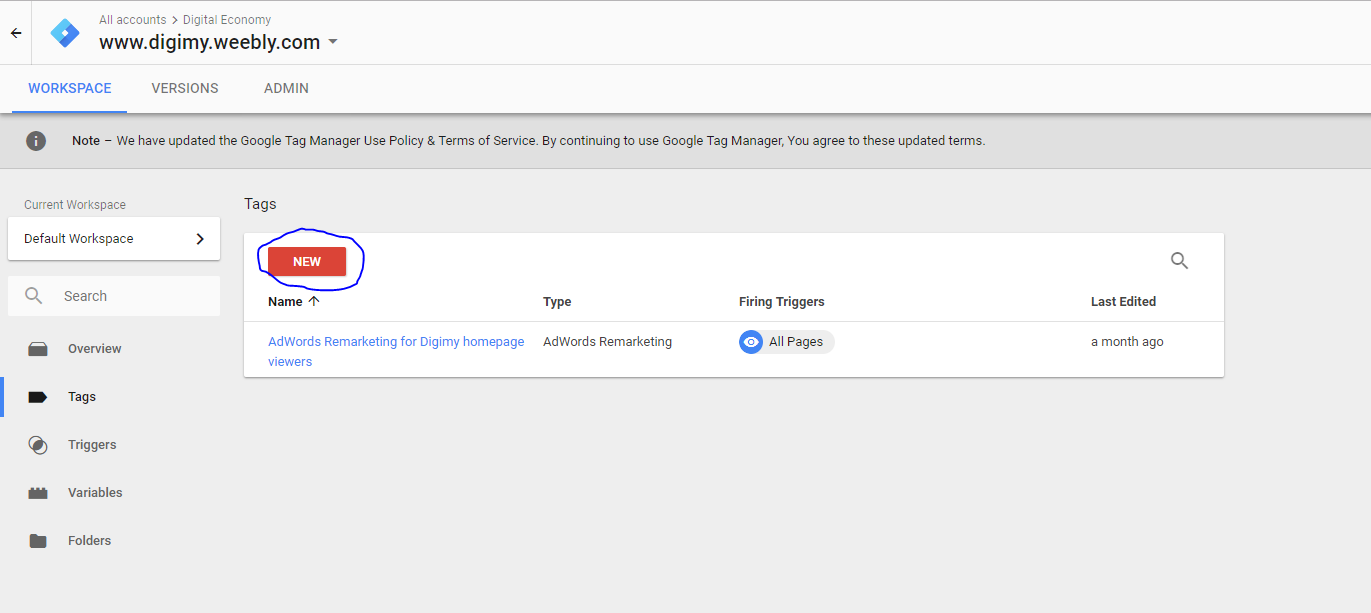

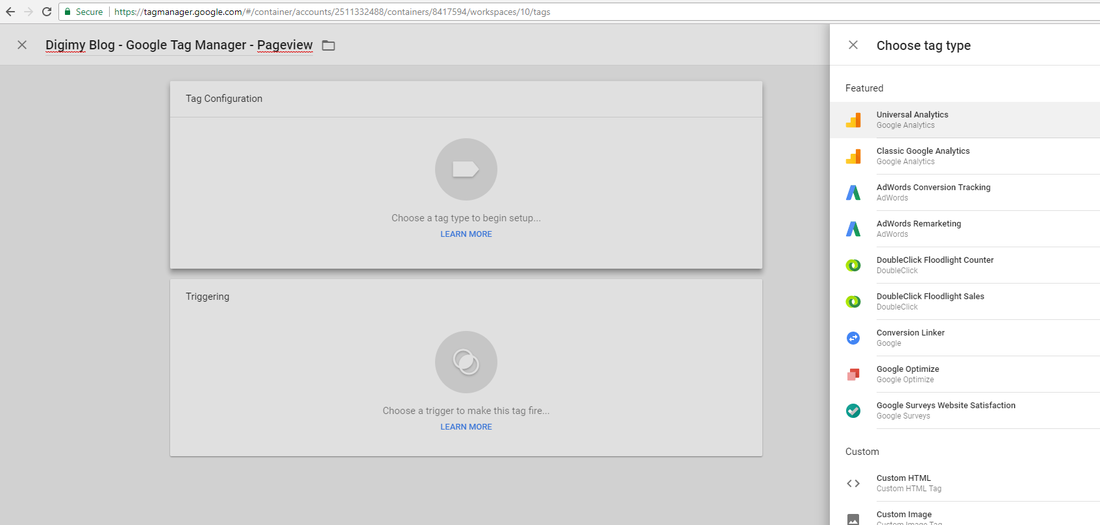

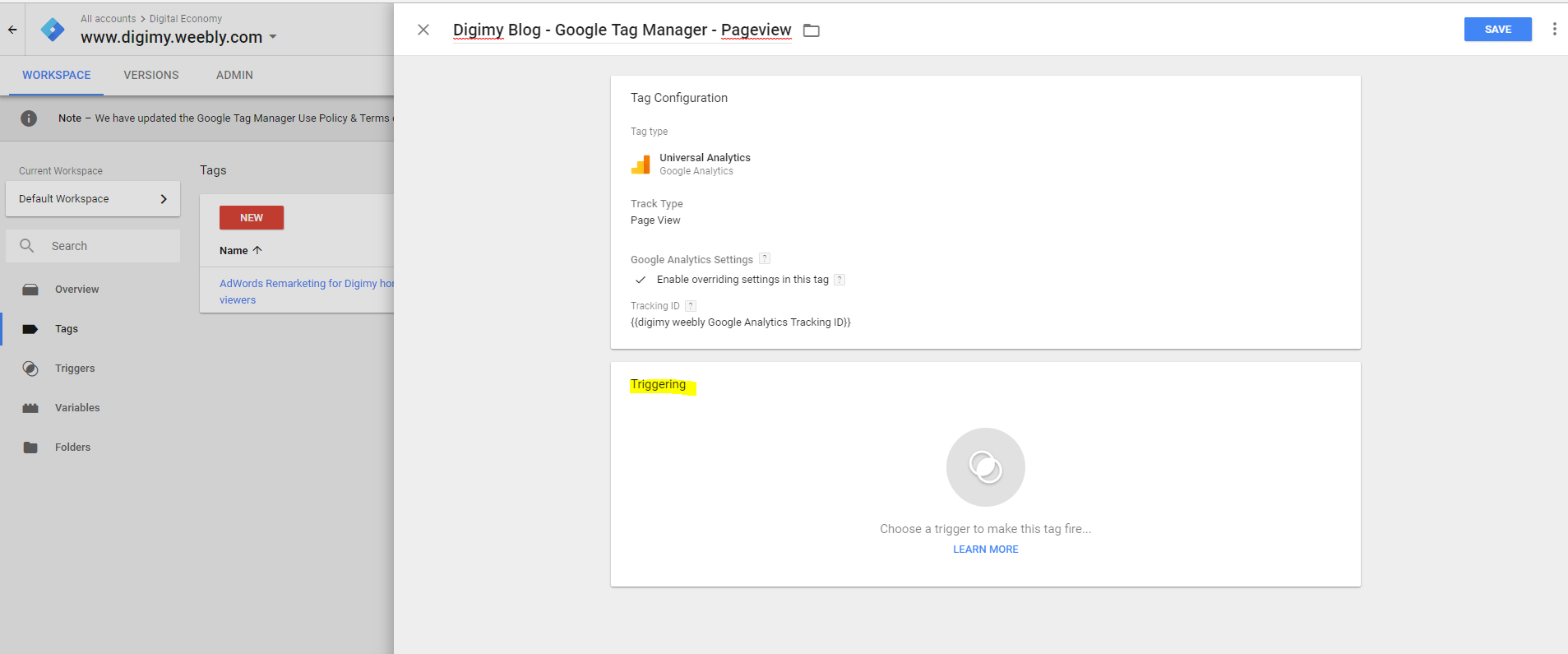

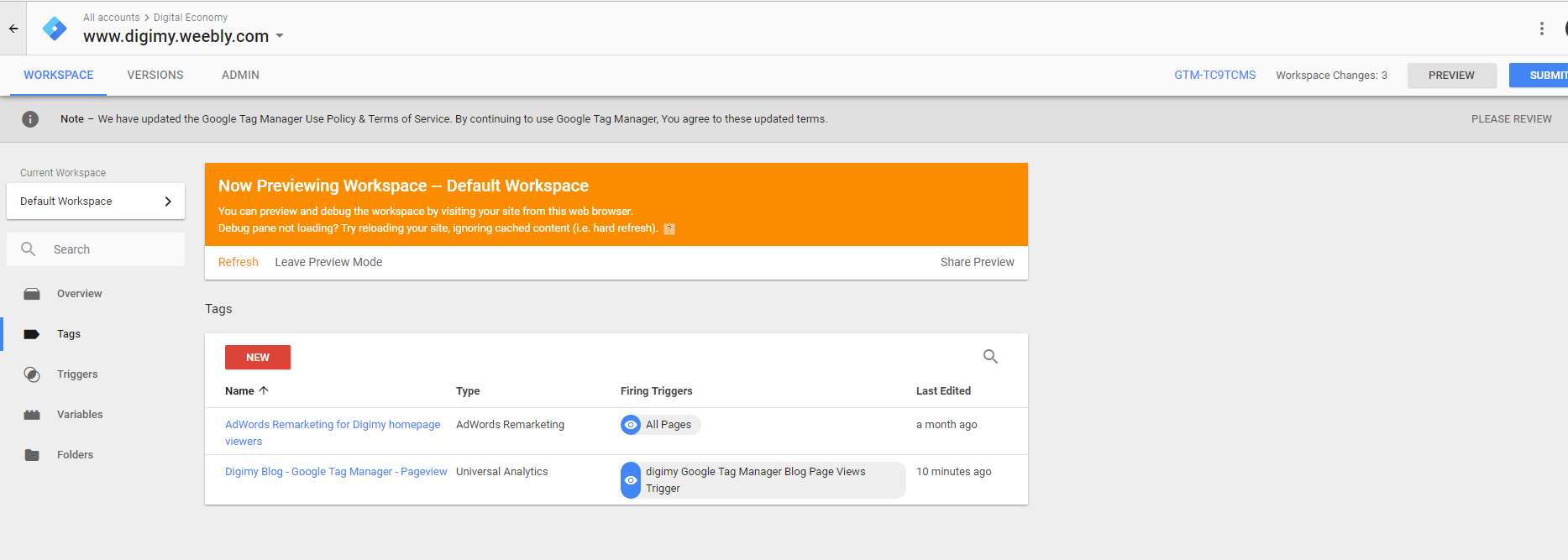

Under Tags, click on NEW as shown below. I want to set up the Tag Manager to monitor pageviews to my Google Tag Manager blog (this blog). Hence, I name it as- Digimy Blog - Google Tag Manager - Pageview

There various Tracking Types. For our purpose of monitoring this blog, let's choose Page View for now.

Check Enable overriding settings in this tag. Click on the icon next to Tracking ID

We will now configure when this Tag will trigger as follows-

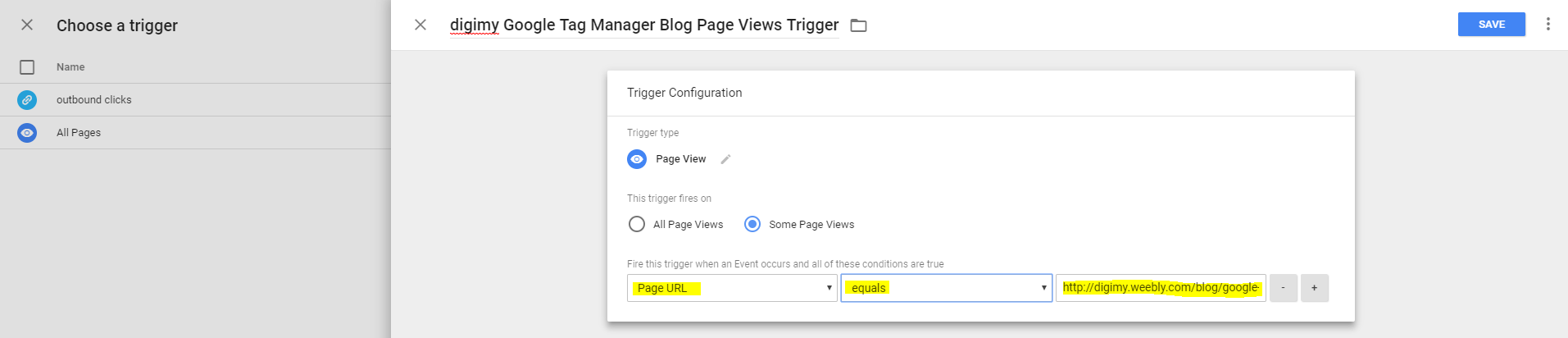

I want to name the Trigger as digimy Google Tag Manager Blog Page Views Trigger.

Select Page View -> Some Page Views and then enter the page URL as follows. Page URL equals <URL>

Click SAVE.

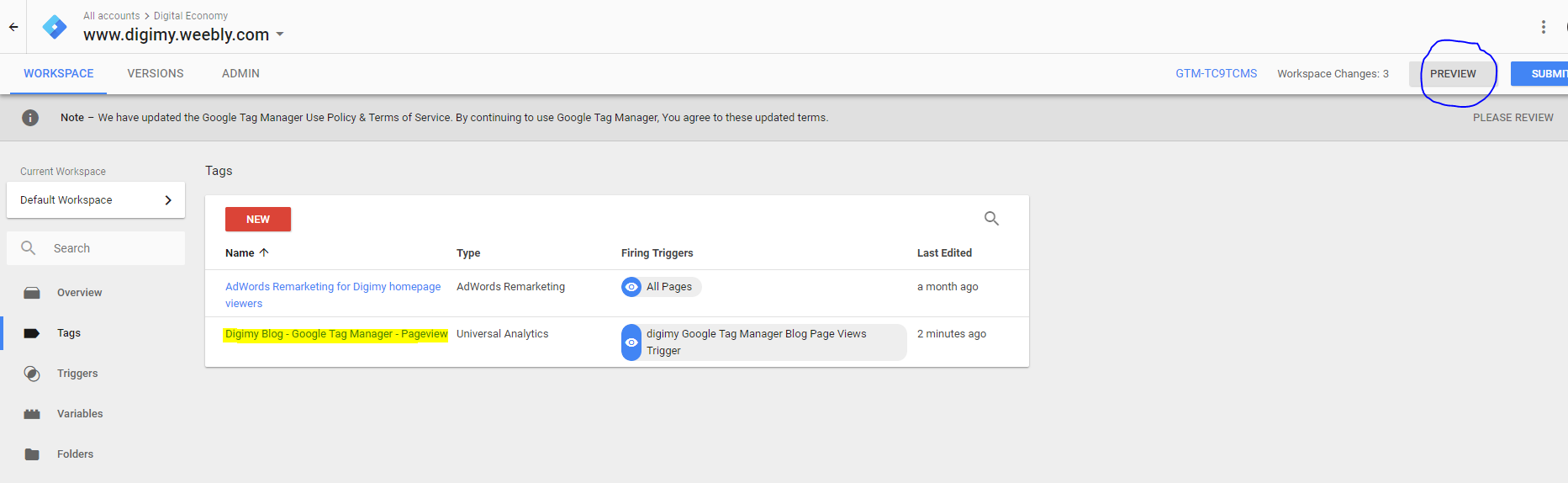

Testing the Tags Triggering in PREVIEW Mode

Let's do a simple test to check if this tag gets triggered. Click on PREVIEW.

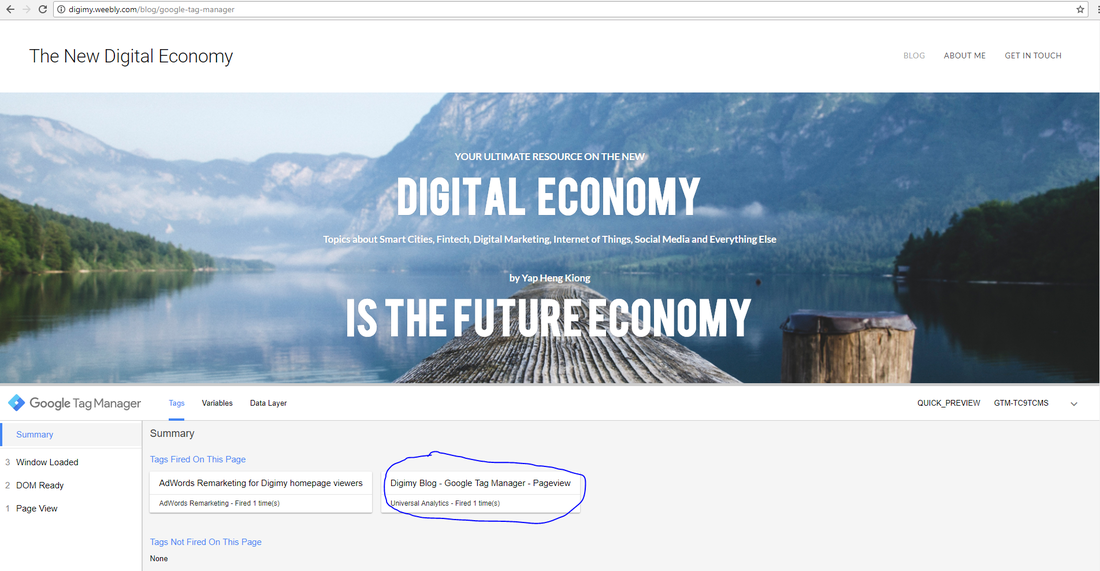

Next, open a new Window and goto the web URL that you have configured to monitor. In my case, that would be

http://digimy.weebly.com/blog/google-tag-manager Because we are in Preview Mode, the webpage opens up a preview window at the lower window as shown below- You should see the correct Tags being fired at this page.

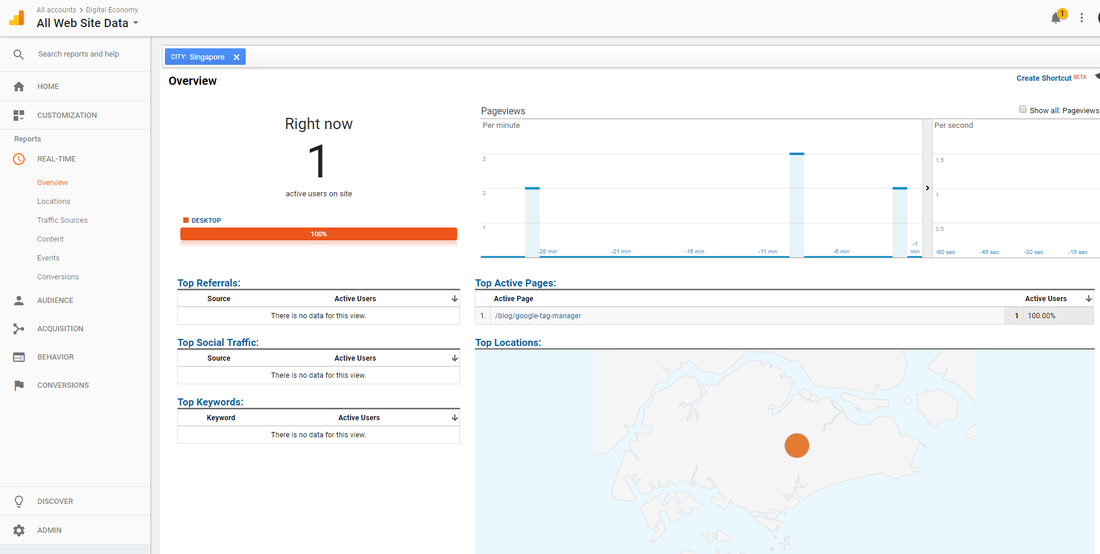

If you head over to Google Analytics dashboard at this time, you should see an active user

Publishing the Tag

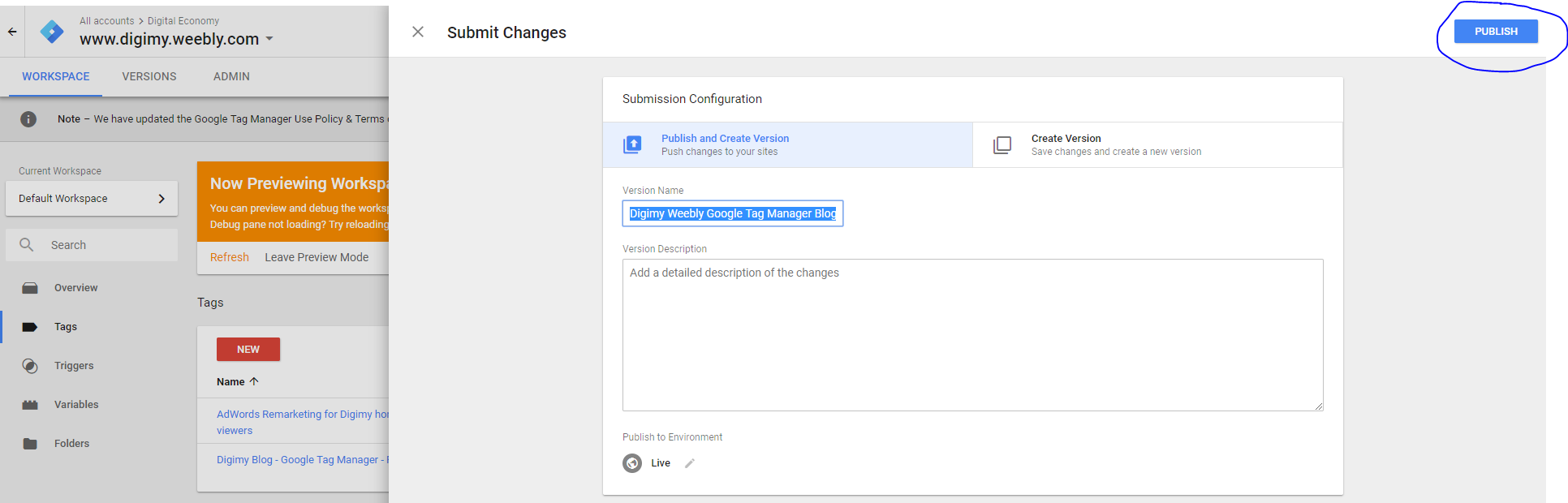

It's time to publish the Tag. Click on SUBMIT.

Enter a name of your choice then click on PUBLISH. In my case, Digimy Weebly Google Tag Manager Blog Page View

This post discusses the Public/Private Key encryption and cryptography technique used in Bitcoin and Blockchain. Follow my other articles to find out more about Blockchain and how it works.

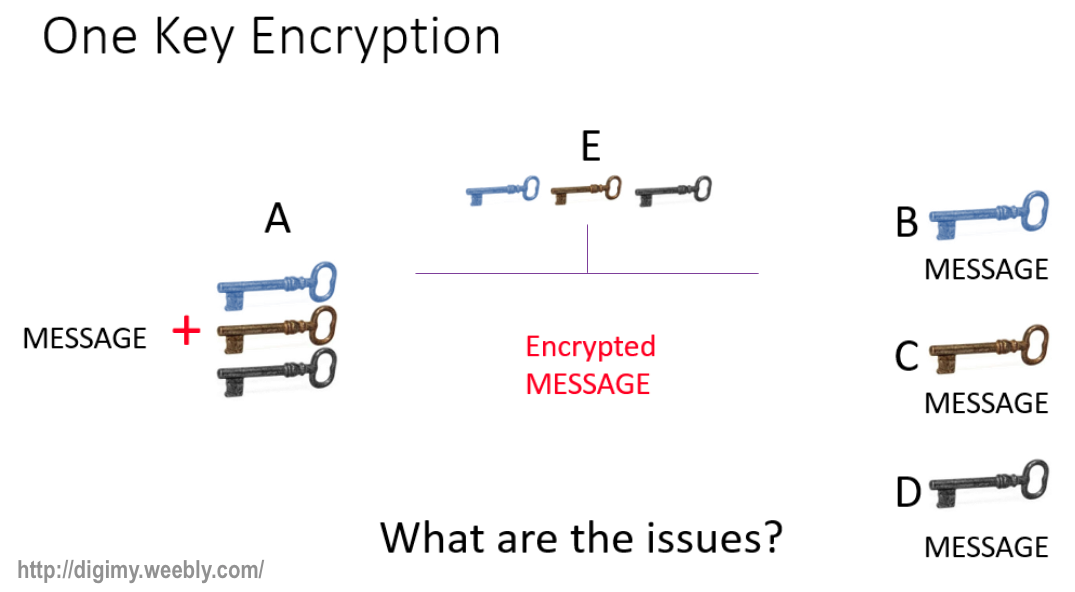

Issues with Symmetric Key System

This is how the One-key (or symmetric) encryption system works. A Sender encrypts the message to be sent using a private key. The private key is then used by the Receiver to decrypt in order to receive the message. The risk of such a system is that anyone else could potentially obtain the private key and able to receive the message though not authorised.

Symmetric Key Algorithm

Symmetric key algorithms are algorithms for cryptography that use the same key for both encryption and decryption.

Plaintext is the unencrypted message whereas Ciphertext is the encrypted message. The issues are:

Encryption Used in Blockchains - Asymmetric Key Algorithms

Blockchain and bitcoin use Asymmetric key algorithms to protect transaction messages across the network.

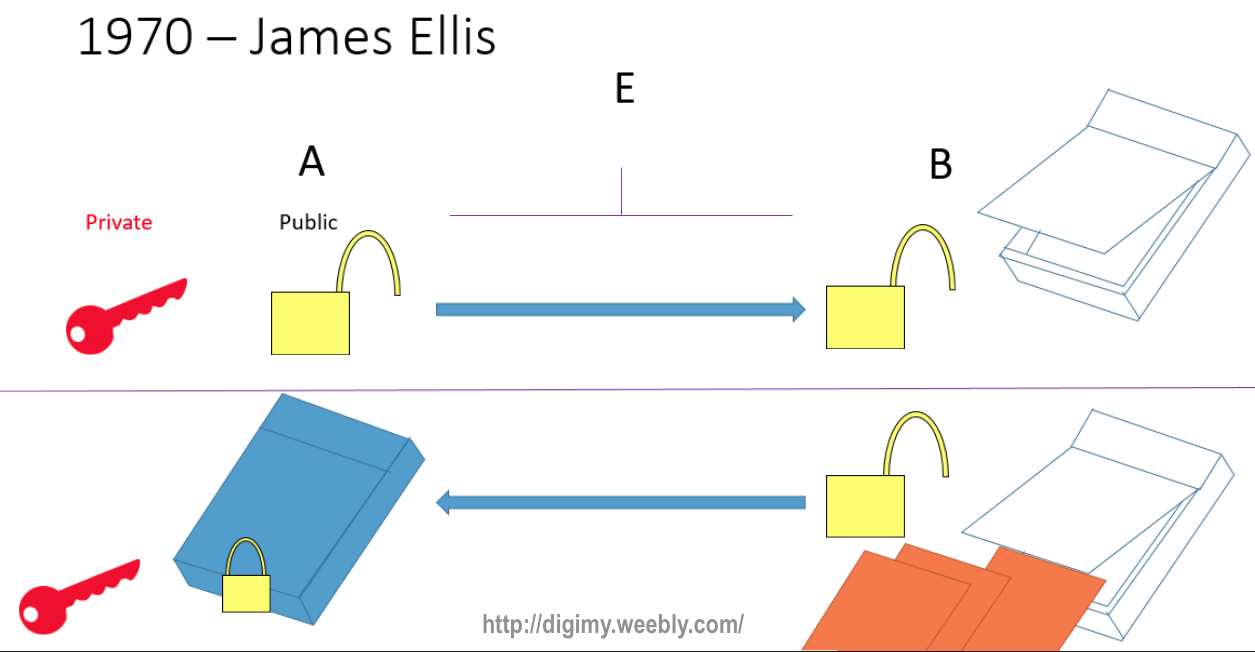

Public key cryptography by James Ellis

James Henry Ellis (25 September 1924 – 25 November 1997) was a British engineer and cryptographer. In 1970, while working at the Government Communications Headquarters (GCHQ) in Cheltenham he conceived of the possibility of "non-secret encryption", more commonly termed public-key cryptography. (Wikipedia https://en.wikipedia.org/wiki/James_H._Ellis)

Instead of sharing a private key, A makes available publicly the lock (public key) which only his private key can be used to open. A then sends the lock to B. B uses the lock to secure and send the message to A. Since the key is private to A, the encrypted message (locked message) will not be subjected to any eavesdropping, e.g. E. Blockchain and bitcoin encrypt transaction messages makes use of public-key cryptography.

How Blockchain works?

How Public/Private Cryptography works?

Clifford Christopher Cocks CB FRS is a British mathematician and cryptographer. Cocks, with his background in number-theory, developed the idea of using prime factorisation to implement Public/Private Key Cryptography, which later became known as the RSA encryption algorithm.

What is prime factorisation? In number theory, the fundamental theorem of arithmetic, also called the unique factorization theorem or the unique-prime-factorization theorem, states that every integer greater than 1 either is prime itself or is the product of prime numbers. (Wikipedia - https://en.wikipedia.org/wiki/Fundamental_theorem_of_arithmetic). For example, 30 = 5 X 3 X 2 589 = 31 X 19 437231 = 859 X 509 The Euler totient function ϕ Based on another theory proposed by Leonhard Euler in 1760, we introduce Euler phi function, written ϕ(n), ϕ(n) is the number of non-negative integers less than n that are relatively prime to n. In other words, if n>1 then ϕ(n) is the number of elements in Un, and ϕ(1)=1. Hence, ϕ(6) = 2 [1,2,3,4,5,6] ϕ(7) = 6 [1,2,3,4,5,6,7] - 7 is a Prime number ϕ(8) = 4 [1,2,3,4,5,6,7,8] ϕ(13) = 12 [1,2,3,4,5,6,7,8,9,10,11,12,13] - 13 is a Prime number There is an interesting pattern we can observe from the Euler totient theory above, i.e. ϕ(n) = n-1 (if n is a prime number).

Blockchain uses the RSA algorithm to send and sign an encrypted message without a separate exchange of a symmetric key,

To see the implementation of Public/Private Key in action, STEP 1 choose two distinct primes P=11 Q=7 STEP 2 Find N; where N is the product of P and Q. N=PXQ=11X7=77 STEP 3 From above Euler totient theory, we know that ϕ(N)=N-1 and since ϕ(PXQ)=(P-1)X(Q-1); we can determine ϕ(N) In number theory, Euler's totient function counts the positive integers up to a given integer n that are relatively prime to n. ... Euler's totient function is a multiplicative function, meaning that if two numbers m and n are relatively prime, then φ(mn) = φ(m)φ(n). (Wikipedia - https://en.wikipedia.org/wiki/Euler%27s_totient_function)

Therefore

ϕ(N)=ϕ(77)=(P-1)X(Q-1)=(11-1)X(7-1)=10X6=60 (Since P & Q are prime numbers) STEP 4 Next, we choose an Encryption Key (e) or the lock(also known as the public key) as illustrated above. e should be a prime number greater than 1 but less than ϕ(N), and the greatest common divisor, gcd(e, ϕ(N) ) = 1 this means e should be coprime to φ(N). In number theory, two integers a and b are said to be relatively prime, mutually prime, or coprime (also written co-prime) if the only positive integer (factor) that divides both of them is 1. ... This is equivalent to their greatest common divisor being 1. (Wikipedia - https://en.wikipedia.org/wiki/Coprime_integers)

The following numbers satisfy the condition 1 < e < ϕ(N) or 1 < e < 60, where e is a prime number.

2, 3, 5, 7, 11, 13, 17, 19, 23, 29, 31, 37, 41, 43, 47, 53, 59. In this case, let's choose 37 as e. Click on link below to use a tool to find out if gcd(e,ϕ(N)) or gcd(37,60)=1

gcd(37,60)=1

Alternative, here's how to determine gcd

60 = 2 x 2 x 3 x 5 i.e. GCF(37,60) = 1 since there are no common prime factors. In another example 4 = 2 x 2 40 = 2 X 2 X 2 X 5 i.e. GCF(4,40) = 4 (2X2) Therefore the Encryption key (or the lock) is (37, 60). A hides P, Q and ϕ(N); and sends only (e, N) or (37, 60) to B. B has a message to send to A. B uses the Encryption key (or public key) to protect the message (Plaintext) to send to A. A uses a private key (Decryption key) to decrypt the Ciphertext back to Plaintext. The next step shows how the Decryption key is being derived. The Decryption key (d) is derived from and hence is related to the Encryption key (e)

STEP 5

Next, determine d, the Decryption key from the Encryption key (e), which is private to A. (Source - https://www.youtube.com/watch?v=fz1vxq5ts5I)

Since d X e ≅ 1 (mod N)

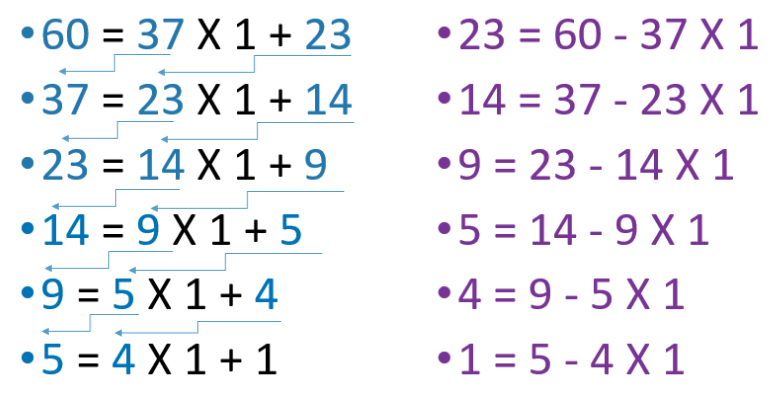

d X 37 ≅ 1 (mod 60) d ≅ 37^-1 (mod 60) 37^-1 (mod 60) = ??

First write down

LHS=60 and RHS=37; Determine the remainder to make LHS=RHS. Hence, 60 = 37 X 1 + 23 Bring 37 and 23 to the left; and repeat the same process above, until you get remainder =1 as shown below.

Once completed, move the numbers around for each line, until you get the following on the right.

Remember we started with:

d ≅ 37^1 (mod 60) 37^1 (mod 60) = ?? Therefore d = 8X60/37=13 Therefore the Encryption key (or the lock) is (37, 60). the Decryption key (or the private key) is (13, 60). Encryption and Decryption of the Message

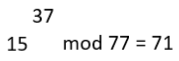

Step 6

To summarise, we have the following: P=11 Q=7 N=11X7=77 ϕ(N)=ϕ(77)=60 e=37 d=13 Assume that B has a message to send to A. The Message, M=15 A sends B the lock (Encryption key): e=37, N=77; B performs the encryption using the following: M^e MOD N = C

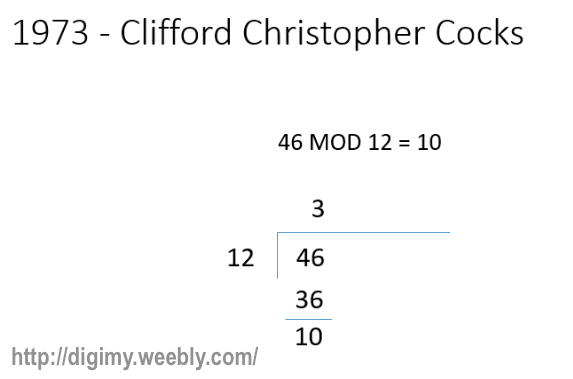

How MOD works?

Step 7

A receives C=71 from B. A performs the decryption using the following: C^e MOD N and get M=15

In actual Blockchain and Bitcoin implementation, P and Q are chosen to be very large numbers.

Resources

https://www.youtube.com/watch?v=O-4_oS3G7MI&t=271s&list=PLoNXVEI2Gdc8CnLo4ceaArsXVoLwWcbj0&index=3

Behold!

Mathematical literacy is not the most important skillsets to work in a bank these days. Thanks to technology and advancements in Fintech solutions that are disruptive to existing jobs and business models.

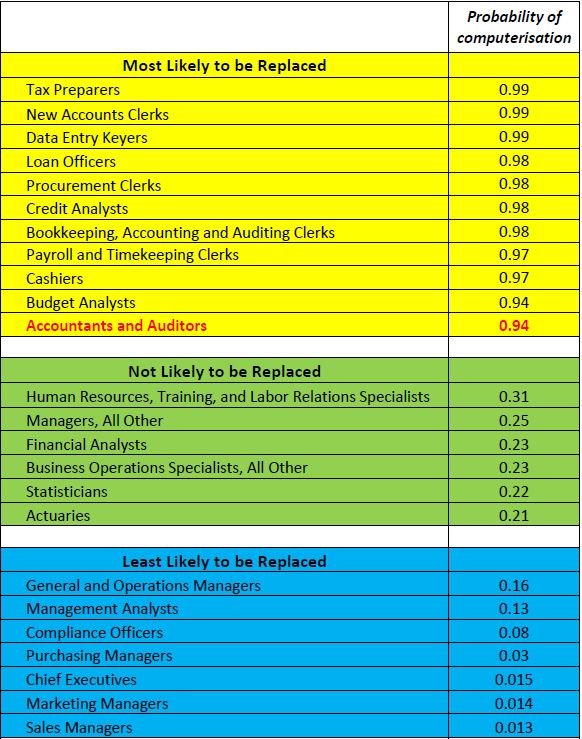

In an article by Anouk Vleugels dated 18 Sep 2017, "Robots will soon do your taxes and your bookkeeper is cool with that", the author presented four examples of solutions that could potentially replace jobs that are susceptible to automation. Occupations like bookkeepers, accounting and auditing clerks could be the most possible ones that are easily replaced.

These solutions include the use of artificial intelligence to either answer questions about possible tax deductions, automate manual and repetive tasks such as streamlining management processes or letting robots review a company’s expense reports.

In another article, "Future of Work: Death of the Accountant and Auditor" the author, Cesar Bacani presented an examination by University of Oxford academics Carl Benedikt Frey and Michael A. Osborne with regard to 702 occupations that are susceptible to computerisation. "The jobs that are at low risk of being replaced by automation include management analysts, compliance officers, marketing managers, sales managers and CEOs."

Sources: The Future of Employment: How Susceptible Are Jobs to Computerisation? and CFO Innovation

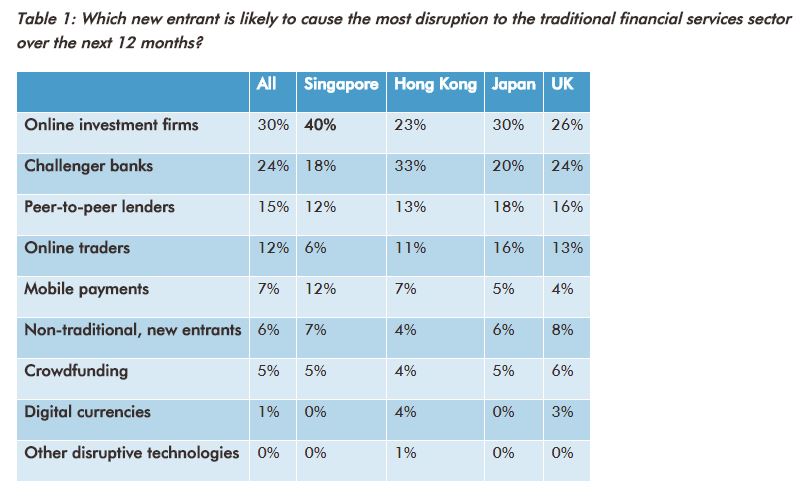

Does the rise of Fintech firms in Asia have the potential to put an increasing number of banking professionals out of work leading to more job losses? After all, Fintech is about making financial services more efficient by increasing its reliance on technology and reducing its reliance on humans. Or will Fintech be actually creating jobs for the banking industry with better prospects? ‘Banks could lose up to 60pc of their retail profits to fintech firms’ Certain jobs being made redundant while new ones are being created

Despite the slowdown in financial sector growth to 0.7% from 5.7% in 2015, The Monetary Authority of Singapore (MAS) noted a net increase of 2,800 financial sector jobs in 2016 in its annual report last week.

The demand for professionals in the areas of finance include compliance, risk management, insurance underwriting, and asset and wealth management. As financial services industry continues to increasingly turn to cyber security, data analytics, network architecture, artificial intelligence, and machine learning to meet the needs in the new digital economy, there continues to be strong demand for expertise in these fields. More banks are pushing new frontiers by embracing and harnessing technology amid the digitisation wave and rise of FinTech, many new jobs, e.g. UX/UI designers, digital data analysts and app developers will be in high demand. Markus Gnirck, co-founder and global COO of Startupbootcamp. “First, jobs which focus on data and information and are mainly done by humans now; and second, jobs involving a lot of repetitive processes.” Embrace change or be engulfed

As Fintechs continue to strive to come up with solutions to poach banking customers and market share, banks are also preparing for the challenges that Fintech poses.

In a highly unpredictable, competitive and dynamic business environment today , workers need to continually upgrade skills to remain relevant. The need for continuous learning and adaptability have never been greater than it is now. Perhaps, no one sums it up better than Jack Ma in this interview with CNBC about Artificial Intelligence vs Human.

Resources

http://www.straitstimes.com/business/banking/singapore-finance-sector-sees-boom-in-tech-jobs-even-as-industry-growth-slows http://www.mas.gov.sg/News-and-Publications/Speeches-and-Monetary-Policy-Statements/Speeches/2017/MAS-Annual-Report-201617.aspx Impact of Fintech to the Banking Industry

The Fintech revolution is fast transforming the way how customers access financial products and services. With the increased use of smart phones and the development of mobile apps, Fintech managed to penetrate the market at an accelerating pace. New products and solutions offered by these Fintech firms have caused the financial sector to experience a good degree of change in recent years.

Just like how Amazon is disrupting the retail industry and Uber to the transportation equivalent, FinTech is gaining significant presence and causing disruption to the traditional banking industry.

An April 2016 article "Fintech is Shaking up the Banking and Financial Services Industry in Singapore", listed the key Fintech ecosystems and their impact on traditional banks and financial services.

Leveraging on technology, Fintech solutions promise easy to use and provide new services at lower cost which banks cannot yet rival.

While banks are counteracting by investing heavily to compete in order to narrow the gap, many Fintech startups are simply willing to operate at a loss in order to gain market share. Challenges which Fintech Companies Face

Many Fintech companies are struggling to justify their high costs of existence. Apart from the cost of people, the relatively high cost of solution development and customer services are pushing Fintech firms to work on tighter budgets.

Besides focusing effort to develop core services and build products to improve the customer experience for financial services, more Fintech startups are struggling to stay on top of their operational costs

No matter how great an innovation is, it will not sell itself. As VC investment into Fintech slowed down, things are becoming tougher for Fintech startups.

As Fintech startups see a pullback in VC fundings, it is becoming more difficult for them to secure new fundings. As mentioned in my previous post, Can Fintech Startups Stay Profitable Without VCs, it is questionable whether Fintech firms are actually profitable. On top of that, most Fintech companies usually provide service-based financial solutions with arguably intangible offerings. Describing their potentials with a clear value proposition and little obfuscation then becomes even more difficult.

The Future of Fintech

So much has been mentioned about the death of banks as consumers are swarming towards Fintech products and services. Banking is transforming itself because of Fintech. The disruption is real. But to claim that banks are dying could just be an overstatement.

In all likelihood, every month you would see a new Fintech startup receiving huge fundings. For every successful one, there are even more Fintech startups struggling everyday just to stay in business. On the other hand, banks are trying their best to win back customer trust. To enable them to stay ahead of their immediate competition and thrive in this period of change, there is plenty of opportunity for traditional banks and Fintech to co-exist. Collaboration between Banks and Fintechs could well be the best way for banks and Fintech start-ups to succeed in this journey.

References

http://www.fintechbd.com/the-challenges-ahead/ https://www.seedrs.com/learn/blog/entrepreneurs/five-challenges-facing-fintech-startups-that-could-provide-big-opportunity https://www.bba.org.uk/news/bba-voice/what-is-the-long-term-impact-of-fintech-on-banking/#.Wb5llEqCzVp http://www.us.confirmation.com/blog/fintech-and-banking http://www.whitlockco.com/fintech-and-your-bank/ https://www.cio.com/article/3148756/leadership-management/the-fintech-effect-and-the-disruption-of-financial-services.html https://www.forbes.com/sites/nikolaikuznetsov/2017/04/07/collaboration-is-the-way-forward-for-banks-and-fintech/#68ecf6a26fdb

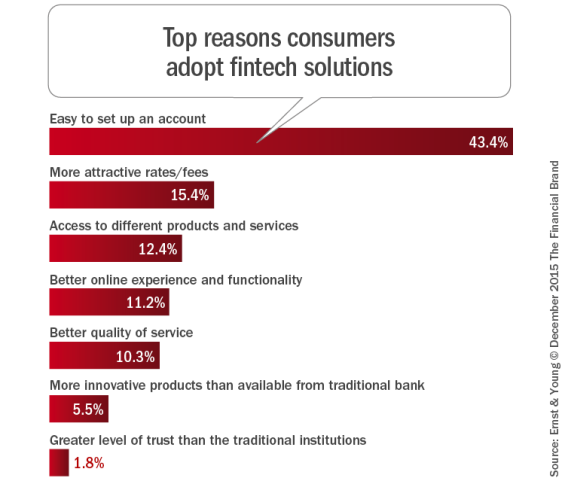

According to the EY FinTech adoption index – Germany Key findings, of the 623 responses, globally, only 1.8% cited trust as the key reason to choose FinTech services over a traditional institution.

Fintech Growth Poised to Disrupt Banking Industry

Many Fintech solutions such as those based upon Blockchains infrastructure and Bitcoin payments have changed how customers access financial services and products. Consumers are being moved away from highly regulated financial services towards more decentralised systems. So does adopting this new Fintech ecosystem really poses no trust and security issues? Or consumers are just so bedazzled by the other aspects of Fintech such as ease of use and more attractive rates that trust and security issues are being neglected? Just this year, I received a SMS alert notice from a local bank informing me of a suspicious transaction of one my credit cards making a purchase online. The transaction, however, did not go through due to the missing credit card verification value. Can such frauds be similarly prevented in Fintech solutions such as Blockchain? Blockchain is the public ledger network which keeps track of the balances for all users and updates them as Bitcoins changes hands. In a decentralised system, consumers need to understand the importance of having greater control over security as no single entity is trusted to verify any form of transactions. This can be seen from the fall of the largest Bitcoin Exchange, Mt. Gox in 2014, which caused the lost of over 460 million dollars worth of Bitcoins, reportedly stolen by hackers. How safe then are Fintech solutions? Since the arrival of social media networking, you begin to realise that every time you engage in an online activity telling people where you are, or asking for recommendations around you, you give up some of your privacy such as your location. Similarly almost all Fintech solutions involve obtaining customer’s private data to generate useful financial insights. Customer's private data are also collected to better predict customers' needs and to provide better user experience. Can Fintech companies provide better customer experience and yet able to protect their customers against cyber threats? Fintech companies are increasingly gaining more control over their customers' financial information and data through the use of technology. To help Fintech companies better protect their stakeholders, more are adopting higher protection such as multi-factor authentication and One-Time-Passwords to minimise the overall risk.

With fast growing popularity of Fintech solutions, the financial services industries are well becoming a major target for cyber crimes. The challenge facing most fintech companies just like the other financial institution is how to keep the customer’s data secure. Fintech solution providers should focus more on risk management and making sure that Fintech business is secured enough to ensure safe banking and financial services are delivered.

Resources:

http://www.techbullion.com/safe-fintech-ecosystem-infrastructure-money-markets/ https://www.wired.com/2014/03/bitcoin-exchange/

In June 2016, Number26 (N26) issued standard account cancellation notices to several hundred customers based on what is known as a Fair-Use Policy. N26 is a Digital-only bank with a full banking license to operate in Europe.

In the email notices sent to their customers, N26 cited, amongst justifications such as suspicious activities, customers using their services too much as being the reason for their account closures.

In another article, "Here's the huge question facing fintech startups - can they make any money?", the author questions the profitability of these Fintech startups. Many startups charge low transaction fees or zero commission in their attempts to capture market size and increase revenue. Have Fintech companies such as N26 reached a point where the highly subsidised service fees can no longer sustain their business?

The business models of most Fintech startups are in collecting transaction and service fees, through payments, lending and investments, and/or commissions by referring customers to business partners.

Most Fintech startups, though offering new products and services over newer platforms such as the Internet and mobile apps, still incur transfer and debit costs just like the traditional financial services. Hence, if even bigger Fintech startups aren't making real profits, what can the other Fintech startups do to overcome challenges to stay profitable? Are these Fintech startups trying to grow as big as they can, and then later try to make money from the customers they have captured?

Benoit Legrand, fintech head of Dutch bank ING, told BI earlier this year: "They’re flourishing everywhere but we’re still waiting for the business model to show up. Where is the money? Where is the return?"

In a heavily regulated banking industry, are Fintech startups able to lower costs and maintain profitability and growth? Otherwise, is it only VC money that's keeping some of the fundamentally flawed business models to carry on business as usual?

Most Fintech startups don't make real money. However, we need to ask ourselves, is profitability the sole purpose of all Fintech businesses? There are thousands of Fintech startups at various stages out there. So what do VCs look for in a Fintech startup company when it comes to potential investment? Some VCs only seek for startups with promised 100X returns, while others may look at startups with potential for significant growths. To stay profitable even without VC fundings, Fintech startups need the right business model. The million dollar question everyone is asking, is, "What is a right business model?" There is no doubt that the Fintech ecosystem will still continue to grow and cause disruption to the traditional banking and financial services. This disruption will be meaningful if it is able to make positive impacts, such as by bringing financial services to the un-bankables or delivering banking convenience to the communities that would otherwise be left out. However, when the reality of profitability sets in, the sustainability of such Fintech startups remains a question for all.

References:

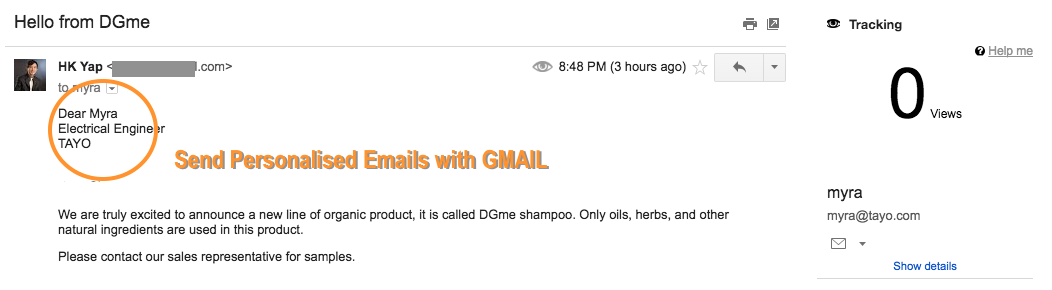

http://uk.businessinsider.com/how-can-fintech-make-a-profit-number26-monese-2016-6/?IR=T http://www.businessinsider.com/fintech-profitability-report-2017-5/?IR=T https://techcrunch.com/2016/07/21/number26-is-now-a-true-bank-as-it-now-has-a-full-banking-license/ Personalised Emails?

Send personalised emails with Gmail

Companies today still rely on the use of opt-in email marketing campaigns to boost sales.

Most businesses send to thousand email recipients using cc or bcc, however, the effectiveness of such emails is incredibly low. Recipients of your emails on the cc or bcc lists are likely to view your emails as spams. Hence, it is definitely better to sign up for a professional newsletter service. These professional services allow you to send personalised emails with your contacts' details and preferences for increased engagement.

Free Tool to Send Personalised Emails using Gmail

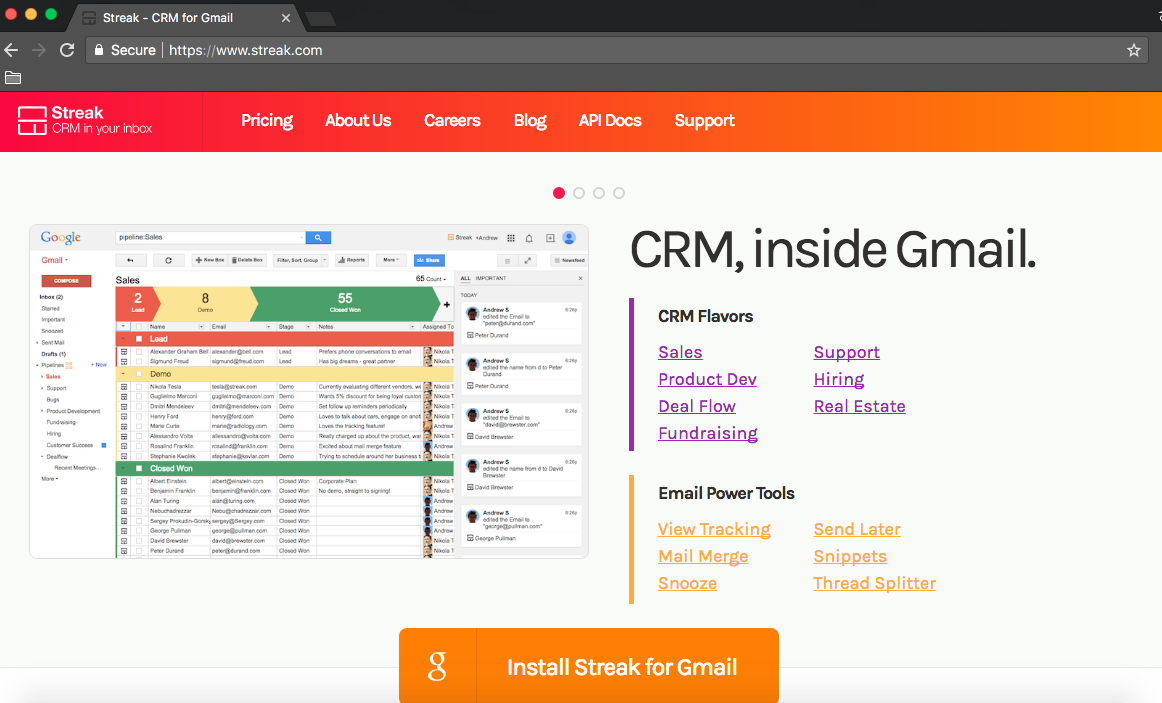

If you are using Gmail, you could consider using Streak to send such personalised emails. Streak is a Google Chrome add-on which transforms your Gmail into a suite of CRM tools.

Streak is based in the cloud and allows businesses to manage sales and customer relationships directly inside Gmail via an Google Chrome addon. Streak lets you manage your sales pipeline inside Gmail. run your entire Sales process right inside your inbox. so you can capture your sales deals and extends existing Gmail into a flexible, fully featured CRM. Mail Merge and View Tracking are two powerful features of Streak.

To start using Streak, visit www.streak.com and install Streak using Google Chrome.

Install Streak for Gmail

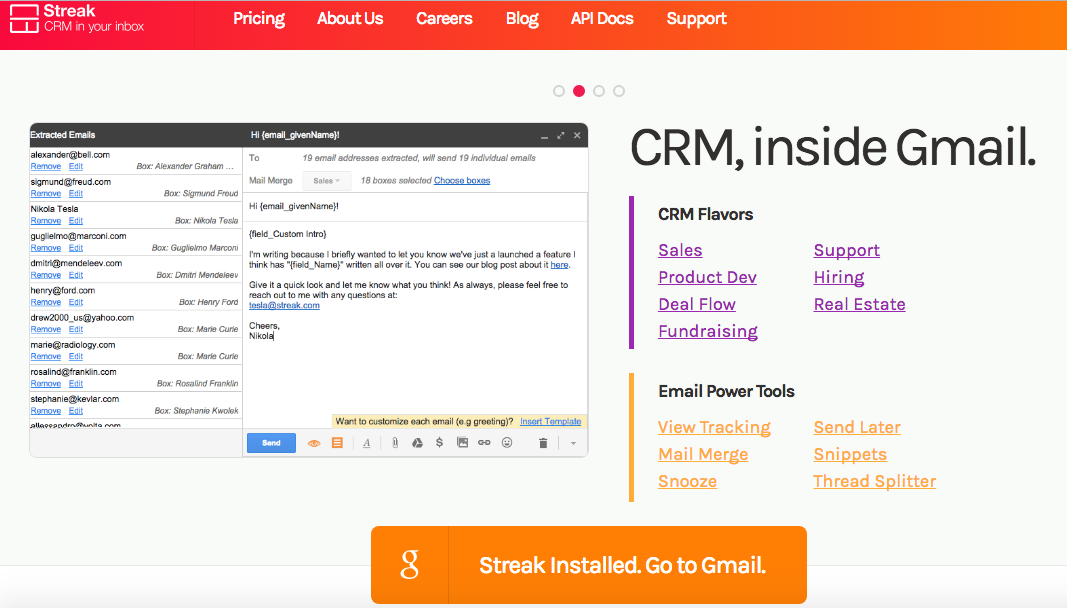

Streak installed in Gmail

Once installed, you are ready to go. Click on 'Streak installed. Go to Gmail'

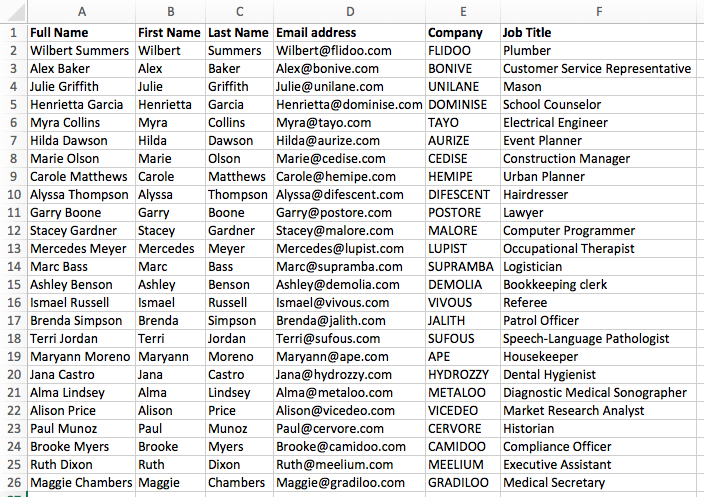

Suppose you keep a record of your contact details in an CSV file as shown below. Let us now go through the steps of importing this list into Gmail installed with Streak.

Sample Contact Details

Random names by of http://random-name-generator.info/

Random business names by http://www.businessnamegenerators.com Random job titles by https://www.randomlists.com/random-jobs  Compose in Gmail Compose in Gmail

Click 'Compose' as you would normally do in Gmail to write a new email.

Watch the screen recording below on how Mail Merge can be easily done with Streak for Gmail.

screen record - sending personalised emails using Streak in Gmail

Yes! That's how easy it is to send personalised emails with Streak.

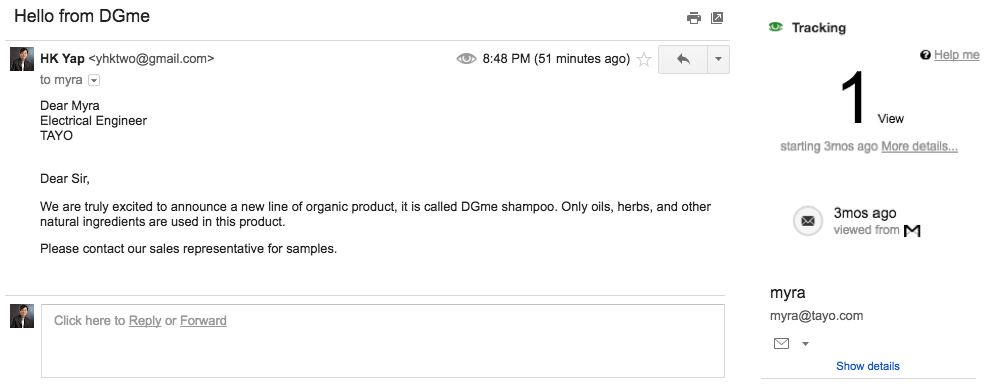

You can even keep track of your emails read status easily within Gmail.

Track Your Website's Performance

Google Search Console

Most of us are aware of using Google Analytics to measure (and analyse) the traffic on your site. However, not all are aware that Google has another free tool known as Google Search Console (previously Google Webmaster) that helps you monitor and maintain your website's presence in Google Search results.

Set up Google Search Console to track your website's performance by clicking on 'Add a property' as shown above. Follow the instructions to add the website URL address you wish to track into the entry box.

Add a property in Google Search Console

Google Search Console -> Add a property

Once Google has started to index your website's pages, you can check indexing status and optimise visibility of your website using Google Search Console.

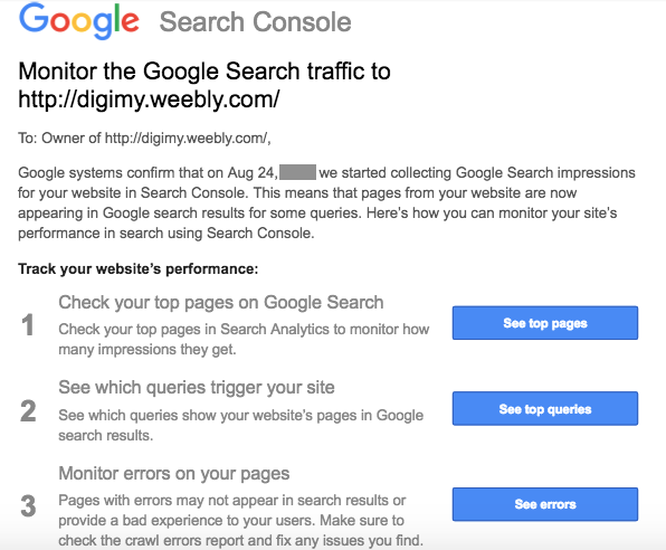

Below shows the the email sent from Google Search Console after successful set-up.

Follow the instructions in the email by clicking on the first link.

Monitor the Google Search traffic - Google Search Console

1. Search Analysis - Top Pages

Track Your Website's Performance

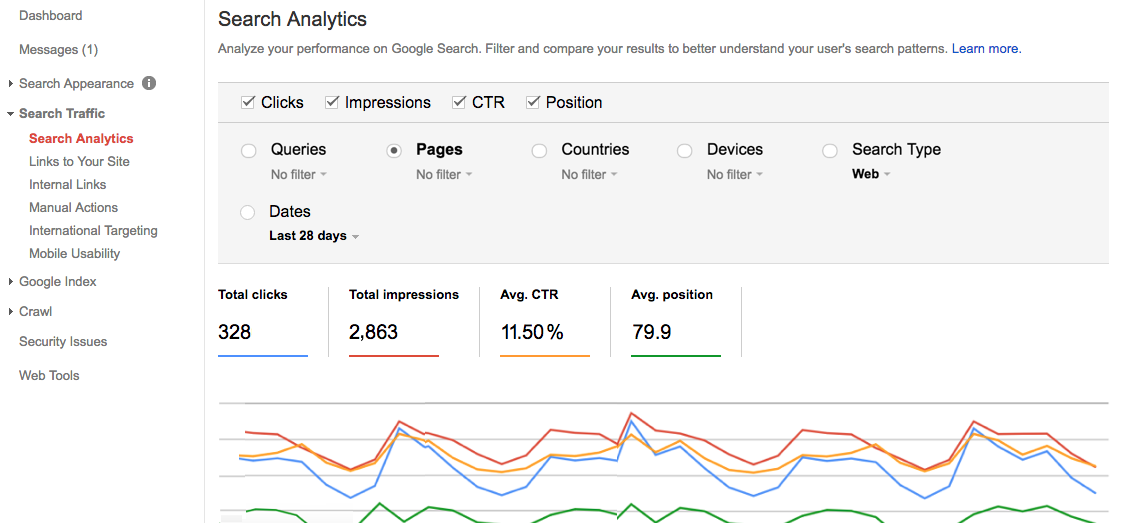

Click on the first item, which is Search Analysis - Top Pages to view number of clicks, impressions, CTR and Average Position of your site pages

Check ALL tabs under 'Clicks', 'Impressions', 'CTR' and 'Position' to view the performance of your website pages.

For more information regarding Click-Through-Rate (CTR) and other online performance measurement metrics, please visit my other post 'Understanding Metrics Used in Online Advertisement Campaigns Such As Click-Through-Rate, Cost-Per-Click' here

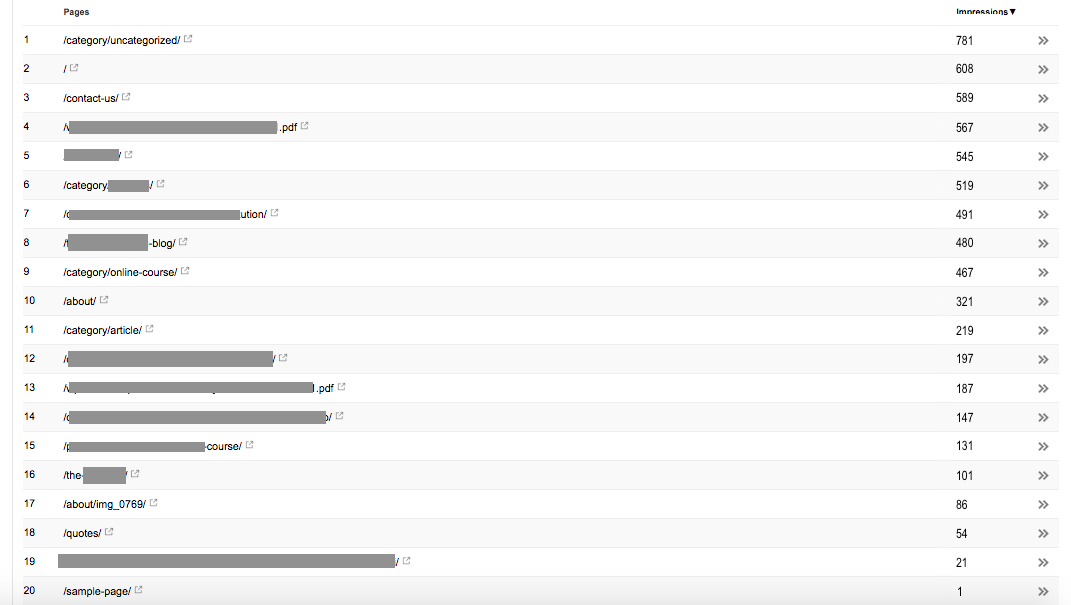

Google Console -> Search Traffic -> Search Analytics filtered by Pages

Next, uncheck all except 'Impressions' to view your top performing pages

Google Console -> Search Traffic -> Search Analytics filtered by Impressions and Pages

Google Search Console -> Search Traffic -> Search Analytics Pages by Impressions

Check 'Clicks', 'Impressions' and 'CTR'

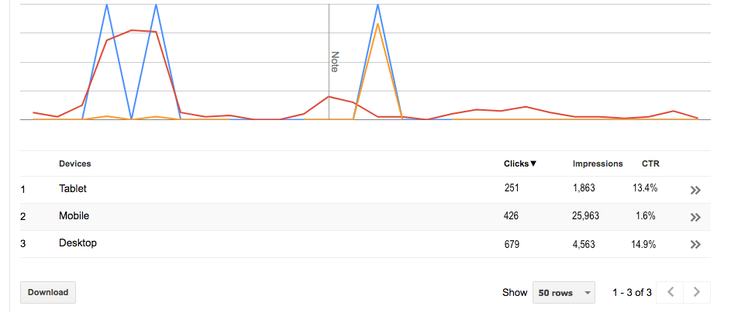

Below is a sample results page showing the same Search Analysis filtered by Devices.

Google Search Console > Search Traffic > Search Analysis Filtered by Devices

2. Which Queries Trigger Your Website

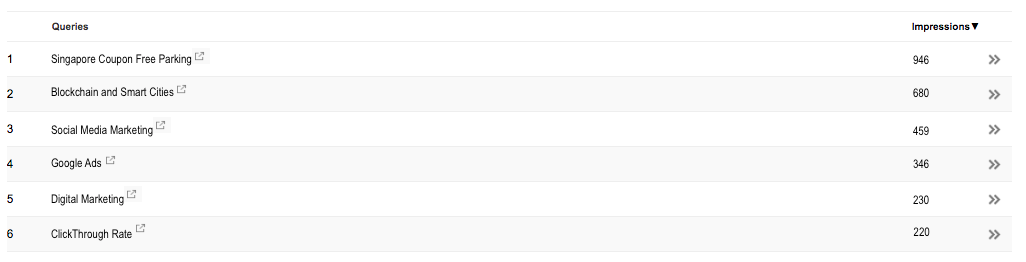

Next, click on the 2nd link in the email from Google Search Console to view results by query strings that users searched for on Google.

See which queries trigger your site

This report allows you to view the query strings that users search for on Google to your website. Obviously, only searches that returned your website will be included.

Are you missing some keywords that you expect to see? These keywords could be missing out from your website content. Which keywords result in high CTR? Which keywords result in high impressions but low CTR? These results help you improve your website content to achieve better outcomes.

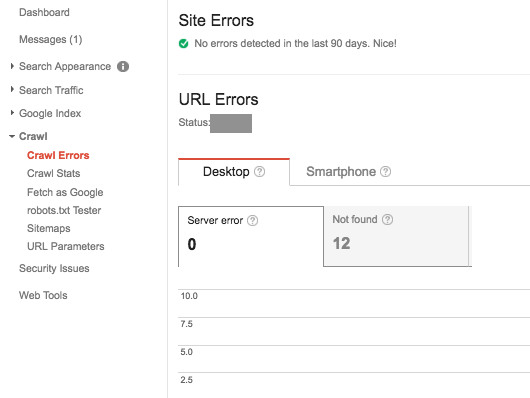

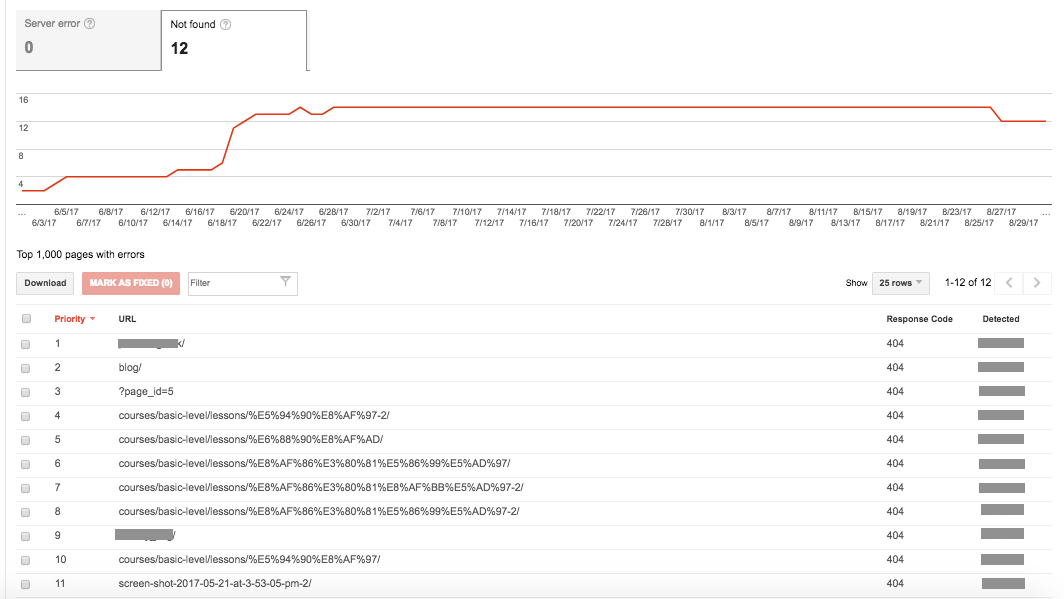

3 Monitor Errors On Your Pages

By default, you will be taken to the 'Crawl Errors' report page. The Crawl Errors report for websites provides details about the site URLs that Google could not successfully crawl.

Two types of errors can be viewed here:

Google Search Console -> Crawl -> Crawl Errors

The most common errors would be 'Not found' (Error 404). Go back to your website editor to fix the 'Not found' errors in the list.

|

RSS Feed

RSS Feed